Streaming wars : Really ?

Finding the battlefield first

Hey Bheem,

In the west, recent media coverage of the Streaming companies have been constructed in a climate of war . I am not so sure about the analogy. And this post is all about why ? Even if we concede to the war analogy, then what about the situation back at home. With different language based industries and over 30 streaming competitors in India, it gets difficult to find an analogy that fits the bill. But, first we bust this war narrative so that we don’t need to find one analogy for our Indian markets in the first place. Read on.

( By clinking the heading you can read this in the browser )

Every major international publication i read in the past few weeks since the launch of “Disney +” on November 1st has been in varying words, tones and ways propagating a war cry. I don’t know nor do i care who is the person that coined this phrase but it clearly makes it look like a massive battle is about to ensue. But, the basic question that none of these pieces are answering is if it really is a war.

To know more, I turned to streaming and digital content expert Mathewball and read through his writings. Also, I remembered a seminal piece from Stratechery about the fundamental difference between a digital streaming company and cable network.

So, instead of covering it all up in a single post, I thought of sparing you and breaking it short and keep this theme going until you have all the angles covered. But to put any suspense to rest, it is not a war. Period.

What is it, then?

It is a shift in the propagation channel of TV ( TV means scripted shows, user-generated content and feature length movies ). This shift is not as simple as replacing your dial-up connection with a broadband. It is slightly bigger and drastic than that. You are not just looking for speed but also opening up for a wide variety of access where everything is only one click away.

So, if that is the case, then what is it that is turning into a commodity. Definitely the content. Right now it has peak demand thanks to the surge of services entering into this business. But, there is a metric that is bound to put a stop to a surge of value of content and that is the viewer’s time.

Also, due to this shift, there are multiple non-production houses that are also entering into the fold. We have the likes of Apple, Amazon and Netflix. Lots of companies from different fields and as being reported many more to come. We need to first understand the building blocks of TV for us to better understand what is at play and how is it going to shape out.

Understanding the Shift

Source: Stratechery

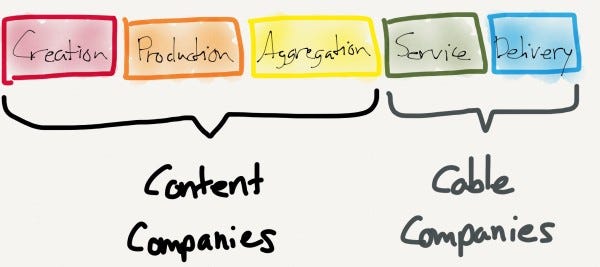

TV can be broken up into five distinct parts:

1. Content Creation is the actual creation, filming, and production of a TV show.

2. Content Production is the commissioning and funding of a TV show, usually by a studio.

3.Content Aggregation is the packaging of several different TV shows into a single offering, usually by a network/channel.

4. Service Offering is the marketing of multiple networks and channels to consumers, usually on a subscription basis.

5. Delivery is the actual transfer of television content into your home.

TV’s part still remain the same in the streaming era as well, but the way they are handled is different compared to the cable era.

Different How?

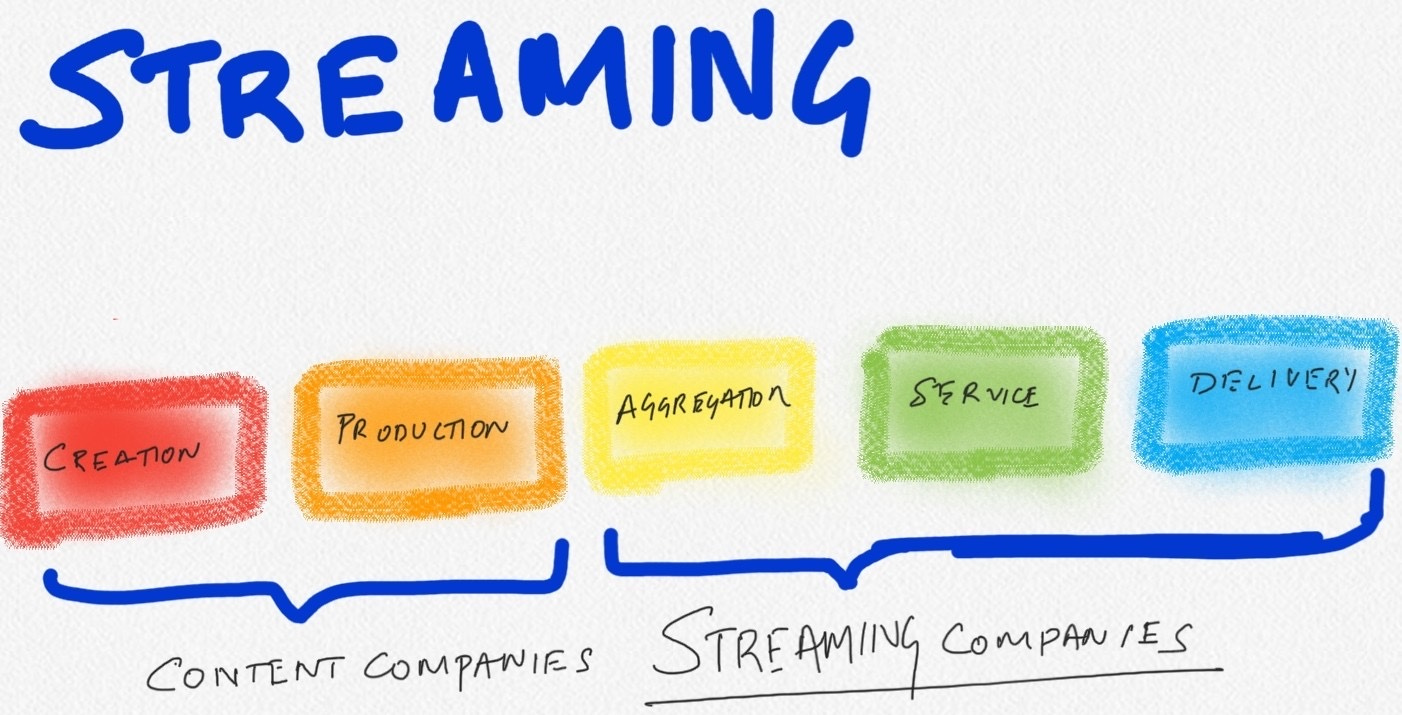

In a cable network, you are viewing only one particular show at a certain time slot. This is what everyone tuning into the channel at that point of time will see. This is flipped on its head when it comes to streaming services. There are no show timings, there is no viewing schedule and you have complete access to the entire catalogue of the service unlike the one show at a particular time in cable channels. This led to consumers seeking content basing upon their preference and only watch shows that they like during times they want and the place they want.

The streaming version of TV looks like this 👇🏽

The content companies are still responsible for creating and producing content whereas the entire process of aggregation, servicing and delivery is taken care of by the streaming companies. This shift is due to the computational revolution of mobile phones, faster internet access with 3G/4G and for lack of a better word, the need for people to feel entertained beyond living rooms.

In theory, this shift looks very easy to explain but it has not been that simple a shift in the first place. With the use of internet, companies require no licenses for delivery of a produced TV unlike in the past where licensing was with cable channel who paid a fee for using the spectrum waves. This resulting in the pool of entrants entering into streaming services also expanding.

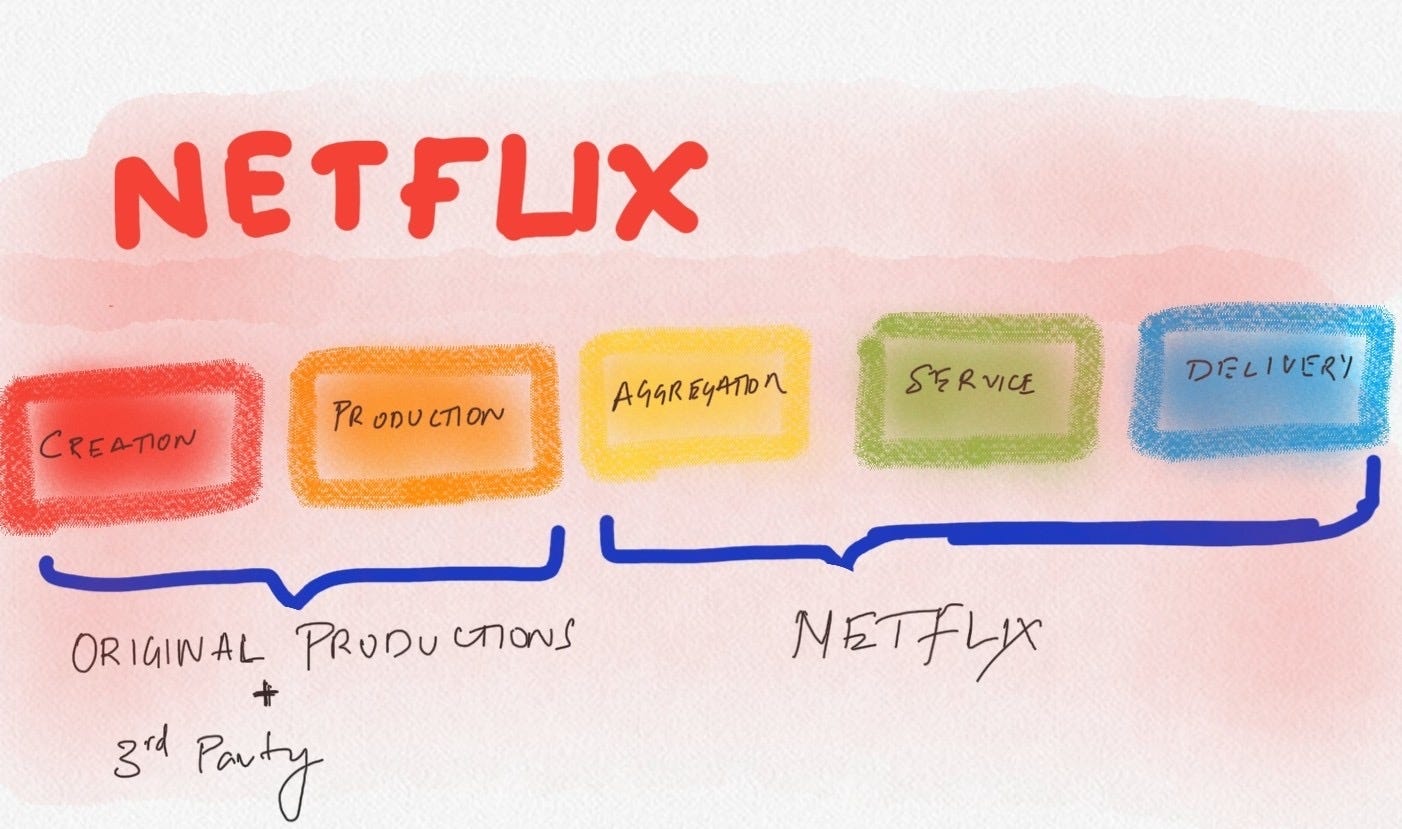

Digital Native: Netflix

We have the pioneering Netflix that was the first to jump on the bandwagon of streaming and waited its turn till the internet caught up to go full fledged into it. Its service’s TV funnel looks like this 👇🏽

For content, they rely on both other content creation companies ( 3rd Party) as well as on heavily building their own original shows where they do the production with various content companies thus practicality becoming a production house in itself. This current year they have invested around $12 billion for their original content.

This heavy spending is due to the entrance of legacy production houses ( NBC, Warner Bros ) into digital streaming and in line with their interests are revoking the access of their content from Netflix.

One such example is the non-renewal of Marvel Cinematic Universe ( Avengers, Iron Man .. )content with Netflix once the contract term expires.

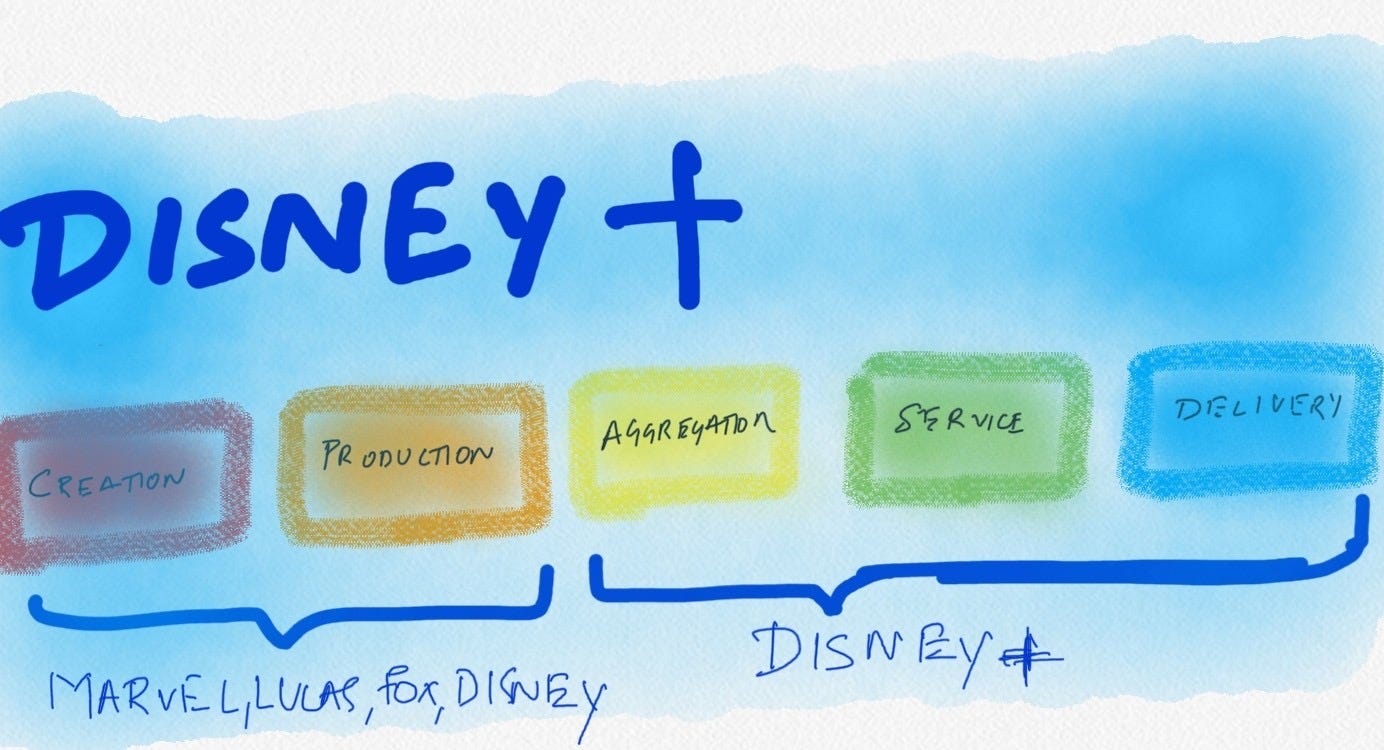

Legacy Content Company : Disney +

Disney is being hailed as the answer to the tech onslaught and a case study in "How to fend off technologies companies". Disney is like the godzilla of content companies as it has most of the top grossing movies in a particular year at box office. In a single day, it amassed 10 million Sign ups for its Disney + service. On the other hand, Hulu(Similar to Netfilx model), a Disney acquired streaming service took 7 years to reach the same stage.

Disney has recently been in an acquisition spree and bought few studio houses. This resulted in basically it owning large chunks of Hollywood TV.

It has some long running franchise IP ( stories and rights on content )like Toystory, Starwars and Marvel Cinematic Universe.

It is like the perfect streaming service if you have kids. It has all the kid friendly shows you will ever need.

This is typical production studio that instead of licencing it’s content to cable companies, now decided to reach the consumer directly as the tv viewing patterns shift in the younger generations.

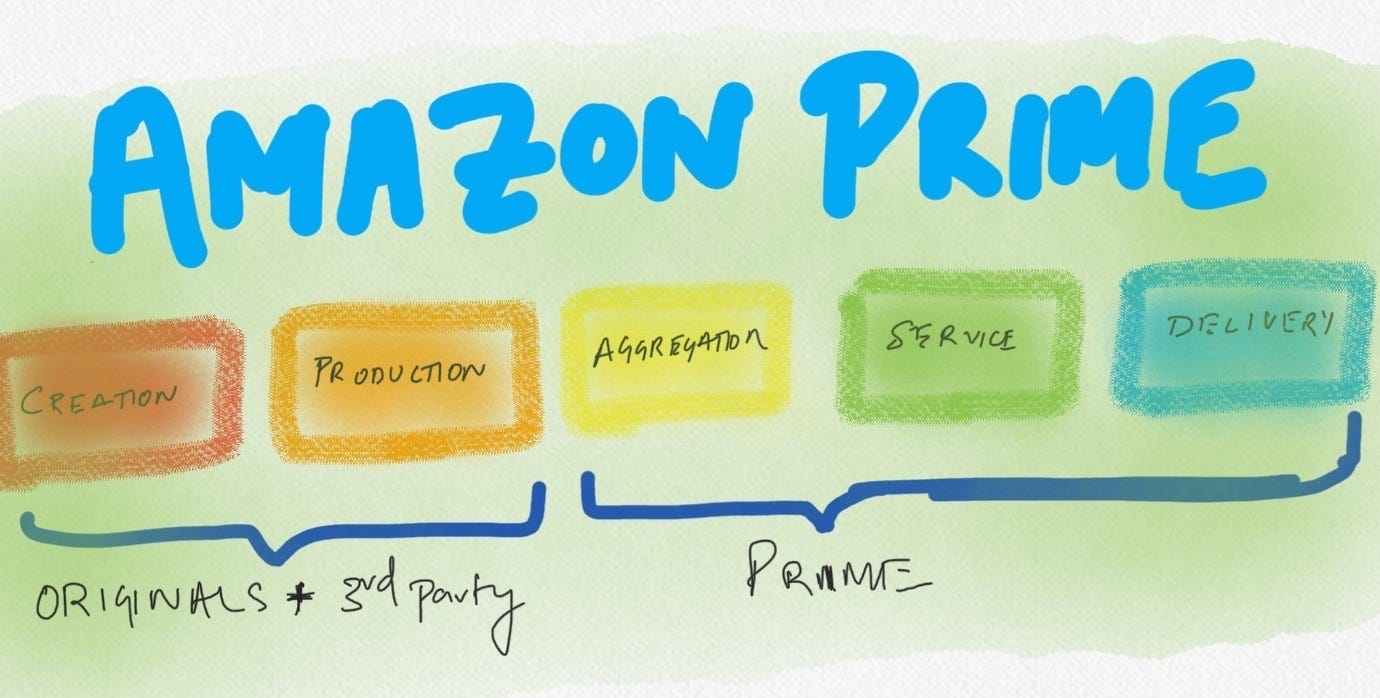

User acquisition channel: Prime Video

I mentioned earlier that because of the shift in the medium of distribution, it requires no license to produce content as the delivery of content is on the internet. The pool of entrants has also increased. One such entity is e-commerce giant Amazon. Since its much prophesied launch of membership program, Amazon Prime, video content has always been in its scope. It launched its streaming service from an earlier avatar in 2011.

With the heating competition in the last couple of years from competing services adding to the lack of heft in the hollywood industry it had to bank on its own content that is produced using Amazon Studio to get some content pouring into its service. Many were duds but in the last year, few of its original shows won the academy awards, changing the tide I suppose.

Until recently, Prime Video comes bundled in the Prime subscription. It still does but you could also subscribe to Prime video separately now.

But, the whole point of Prime subscription is you could subscribe to one membership and also get video content free along with faster e-commerce deliveries. So, technically Amazon is looking to make its offering even more lucrative to prime customers rather than making a business out of its streaming service. This can be termed as user acquisition and user retention costs rather than profit making entitiy.

Narrative Fallacy: A media ploy

Which brings us to the Streaming Wars that have been declared by the journalists while covering these companies and their launches. There are even more companies that are entering into the space like AT&T which owns Warner Brothers and HBO, and NBC which is owned by Comcast. These are basically cable companies taking their own content companies to shift to the newer medium of distribution. I won’t go much in to depth about the value proposition they are looking to provide to customers but all they are offering is their own content for users to access on any of their devices using the internet.

Going by the way TV is produced what we are witnessing is not some unique innovative disruption, rather what we are witnessing is the flocking of varying brands on to the new medium. This doesn’t fundamentally add anything new to the already recognised fact that internet can be the default mode of distribution for all types of content and services.

The forming of the narrative as a war defeats the shift that is being undertaken. And that shift has a completely different meaning and challenge when it comes to India. Especially in India, where everything and everyone has space to grow. Where both the legacy, in this case the cable networks and the streaming services are having huge headrooms to grow in their respective mediums. Where there are regional industries and people are watching more and more content on their phones. Things get interesting when a company is looking at this unique market and decide to enter and try to win it. More on that in future posts.

Closing words

Every entrant into the streaming space has their own motivations to start a service but this comes at a cost. What is the cost each one is ready to pay and why? This will be interesting to find out.

While all the focus is on entrants, there are still a whole set of problems that are plaguing this space. The likes of bandwidth speed, preferred devices, content preferences, underlying tech that is delivering the service, discoverability( User experience), user fatigue and content shelf life. I could keep going on but as mentioned earlier, all of these for later posts.

Regards,

Vivek

The Duologue is an effort by Vivek and Bheem to have a dialogue about varying topics.

If you liked what you read, you can subscribe to our newsletter.

Share it around if you find any of this piqued your interest or might be interesting for your peers.